How To Choose The Best Private Business Loan For Your Education

Business Loan Choosing the best private student loan is a crucial decision that can affect your financial future. Unlike federal student loans, private loans come with different interest rates, terms, and repayment options. Here’s a guide to help you navigate the process and find the best private student loan for your education.

1. Understand the Basics of Private Student Loans

Private student loans are financial products offered by banks, credit unions, and online lenders to help students cover their education-related expenses, Business Loan such as tuition, fees, books, and living costs. Unlike federal student loans, which are funded by the government, private student loans are provided by private institutions and can vary widely in terms of interest rates, loan terms, and eligibility requirements.

Here are the key aspects to understand about private student loans:

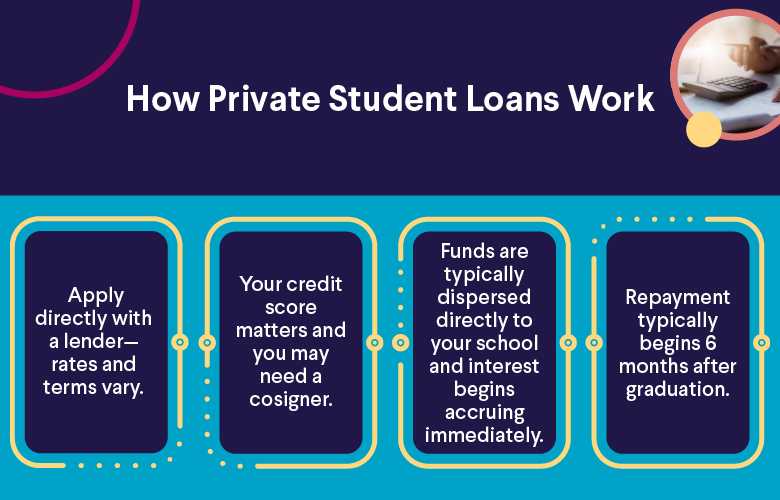

How Private Student Loans Work

Private student loans are typically borrowed by students to fill the gap between the cost of their education and the amount covered by federal student loans, scholarships, and grants. These loans can be used for any education-related expense, including:

- Tuition and fees

- Room and board (on-campus or off-campus living)

- Books, supplies, and other educational costs

Private student loans are typically credit-based, meaning that lenders will evaluate the borrower’s creditworthiness when deciding whether to approve the loan and at what interest rate. This is a key difference from federal student loans, which are not credit-based and are available to most students regardless of their credit score.

Here’s a table that outlines the key aspects of private student loans to help you understand the basics:

| Aspect | Details |

|---|---|

| What Are Private Loans? | Loans provided by private lenders (banks, credit unions, or online lenders) to cover education costs. |

| Eligibility | U.S. citizenship or permanent residency, enrollment in an eligible degree program, creditworthiness. |

| Credit Check | Private loans are credit-based, meaning lenders evaluate the borrower’s credit score. A cosigner may be required for those with limited or poor credit. |

| Interest Rates | – Fixed Rates: Stay the same throughout the loan term. |

pgsqlCopy - **Variable Rates**: Can fluctuate based on market conditions, potentially increasing over time. |

2. Compare Interest Rates

When evaluating private student loans, one of the most important factors to consider is the interest rate. The interest rate determines how much you’ll pay on top of the amount you borrow, so it can significantly affect the total cost of your loan over time. Here’s a comparison of the different types of interest rates you may encounter with private student loans:

| Interest Rate Type | Description | Pros | Cons |

|---|---|---|---|

| Fixed Interest Rate | The interest rate stays the same for the entire loan term. | – Predictability: Monthly payments remain the same throughout the loan term. | – Initial rates may be higher than variable rates. |

| – Easier to budget and plan for the future. | – Less flexibility if interest rates decrease. | ||

| Variable Interest Rate | The interest rate can change over time, typically based on an index (e.g., LIBOR or SOFR) plus a margin. | – Initial rates tend to be lower than fixed rates. | – Monthly payments can fluctuate, making it harder to budget. |

| – Potential for lower overall interest costs if rates remain low or decrease over time. | – Risk of rising rates, leading to higher monthly payments. | ||

| How Interest Rates Are Determined | The interest rate depends on factors such as the borrower’s credit score, the loan term, the lender’s policies, and whether the loan has a cosigner. | – Creditworthy borrowers may secure lower rates. | – Borrowers with poor or no credit may face higher rates or need a cosigner. |

| Interest Rate Range | – Fixed Rates: Typically range from 5.00% to 12.00% (depending on credit and loan type). – Variable Rates: Typically range from 3.00% to 10.00% (depending on credit and loan type). | – Borrowers with strong credit scores or cosigners may access the lowest rates. | – Borrowers with poor credit may face higher rates. |

| Interest Rate Impact on Repayment | A higher interest rate means higher monthly payments and more money paid over the life of the loan. | – Fixed rates provide stability, while variable rates offer potential savings if rates decrease. | – A higher interest rate increases the total cost of borrowing over the long term. |

Key Factors Affecting Interest Rates:

- Credit Score: Lenders use your credit score to assess your ability to repay the loan. Higher credit scores typically result in lower interest rates. If you don’t have a strong credit history, consider applying with a cosigner who has better credit to help lower your rate.

- Loan Term: Loans with shorter terms generally have lower interest rates compared to longer-term loans. However, while the monthly payments will be higher on a shorter-term loan, the total amount of interest paid over the life of the loan will be lower.

- Cosigner: Having a creditworthy cosigner can help you secure a lower interest rate, especially if your credit is less than stellar. Some lenders allow you to release the cosigner after meeting certain criteria, such as making 24 consecutive on-time payments.

- Lender Type: Different lenders (e.g., banks, credit unions, online lenders) offer varying interest rates, so it’s important to shop around and compare loan offers from multiple institutions. Credit unions often offer competitive rates compared to traditional banks.

- Market Conditions: Interest rates on variable rate loans are often influenced by broader economic factors, such as the Federal Reserve’s interest rate decisions. If market rates rise, your interest rate and monthly payments may also increase.

3. Consider the Loan Terms

Choosing the Right Loan Term for You

When considering private student loan terms, here are some key factors to help you decide which option works best for you:

- Monthly Budget:

- If you need to keep your monthly payments low, you might prefer a longer loan term. However, keep in mind that this will increase the total interest paid over time.

- If you can afford higher monthly payments, a shorter loan term can help you pay off the loan faster and save money on interest.

- Total Interest Costs:

- Shorter loan terms (5–10 years) generally result in lower total interest because the loan balance is paid off more quickly, even if the monthly payment is higher.

- Longer loan terms (15–20 years) may result in higher total interest paid over the life of the loan, even if the monthly payment is smaller.

- Your Future Financial Situation:

- If you expect to have a stable job and income after graduation, a shorter loan term with higher monthly payments might be a good choice.

- If you’re unsure of your financial situation or want more flexibility, a longer loan term with smaller monthly payments could be more manageable.

- Repayment Flexibility:

- Some lenders offer repayment flexibility if you face financial difficulties. You should research whether the lender provides forbearance, deferment, or other forms of relief in case you cannot make payments for a period of time.

- Cosigner Release:

- If you have a cosigner, be sure to check if the lender offers a cosigner release option. If this is important to you, you’ll want to choose a loan that allows for this after a certain number of on-time payments.

4. Check for Fees

Tips for Checking Fees When Choosing a Private Student Loan:

- Read the Fine Print: Always review the loan agreement thoroughly. Ensure you understand all fees associated with the loan, as these can affect the total cost and your ability to repay the loan comfortably.

- Ask About Fees Upfront: Before signing any loan agreement, ask the lender directly about all the fees you might incur during the loan process. Some lenders may not disclose all fees until after you’ve already been approved.

- Compare Lenders: Different private lenders have different fee structures. Some lenders may offer loans with no fees at all, while others may charge multiple fees. Compare terms from several lenders to find the one that offers the most competitive rates and fewest fees.

- Check for Fee Waivers: Some lenders may offer fee waivers for specific circumstances, like setting up automatic payments or having a cosigner. Be sure to inquire about any available discounts or fee waivers.

- Factor Fees into Your Loan Cost: When comparing loans, consider both the interest rate and any associated fees. A loan with a lower interest rate but higher fees may actually cost you more in the long run than a loan with a slightly higher interest rate and no fees.

Example: Loan Comparison with Fees

Let’s compare two private student loans with different fees:

| Loan Option | Loan Amount | Interest Rate | Origination Fee | Late Payment Fee | Prepayment Penalty | Total Fees Over Loan Term | Total Loan Cost |

|---|---|---|---|---|---|---|---|

| Loan A | $20,000 | 6.00% | 1.5% | $35 per missed payment | None | $300 (origination fee) | $26,944.94 |

| Loan B | $20,000 | 5.75% | None | $40 per missed payment | $200 (prepayment penalty) | $240 (late payment fees) | $26,669.52 |

- Loan A charges a 1.5% origination fee ($300) but has no prepayment penalty, making it a more favorable choice if you plan to pay off the loan early.

- Loan B has no origination fee but charges a prepayment penalty and higher late payment fees, which could cost more in the long term if payments are missed.

5. Evaluate Loan Forgiveness and Repayment Flexibility

Key Considerations:

1. Loan Forgiveness:

- Private loans do not offer loan forgiveness like federal loans (such as PSLF) or Teacher Loan Forgiveness. Therefore, you are responsible for repaying the full loan amount, including interest. If loan forgiveness is a priority for you, consider federal loans over private loans.

- Some private lenders might provide limited forgiveness for disability or death, but this is not typical for standard repayment situations.

2. Hardship Forbearance:

- Forbearance can be an important option if you run into financial difficulty and need to temporarily stop making payments.

- Important Note: Interest continues to accrue during forbearance, so the amount you owe can increase during this period. Make sure you understand the terms, especially if you plan to use forbearance as a way to manage temporary financial hardship.

3. Deferment:

- Deferment is typically available for students while they are in school, and it may also be offered in certain cases like military service. However, interest usually accrues during deferment (unless it’s a subsidized loan or specifically stated otherwise).

- Deferment can extend the loan term, which could lead to more interest payments over time. Be cautious when considering deferment, as it can increase your debt.

4. Flexible Repayment Options:

- Some private lenders offer flexibility if you’re facing difficulty making full payments. You might be able to pay only the interest while you’re still in school or use a graduated repayment plan, where your payments start smaller and gradually increase as your income grows.

- Flexible options can make it easier to manage your finances, but always consider how they affect the total amount of interest you will pay over the life of the loan.

5. Cosigner Release:

- If you have a cosigner on your loan, check the terms regarding cosigner release. After making a certain number of on-time payments, you may be able to release your cosigner from responsibility for the loan.

- Cosigner release is an important feature for both the borrower and the cosigner, as it allows the cosigner to be removed from the loan after a period of responsible repayment.

6. Refinancing and Income-Based Repayment:

- Refinancing may help lower your interest rate or monthly payment after you graduate. Keep in mind that refinancing private loans with other private loans means you will lose any potential government protections, such as income-based repayment or federal forgiveness programs.

- Income-driven repayment plans (IBR) are generally not available with private loans, though some private lenders may offer income-based repayment alternatives that can help adjust your payment amounts.

6. Check the Eligibility Requirements

- Credit Score: Most private student loans require a credit check, and the better your credit score, the better your rates will be. If you have a limited credit history, you may need a cosigner.

- Cosigner: A cosigner can improve your chances of getting approved and securing a lower interest rate if you don’t have a strong credit history. Some lenders also offer the option to release your cosigner after a certain number of on-time payments.

7. Look for Discounts and Incentives

- Many private lenders offer discounts for signing up for automatic payments or other incentives like career coaching or financial planning services. These extras can make a big difference in the total cost of your loan over time.

- Exploring discounts and incentives is a smart way to reduce your total student loan cost and make your loan repayment more manageable. Key discounts and incentives include:

- Interest rate reductions for automatic payments, maintaining good grades, or signing up for loyalty programs.

- Cosigner release incentives after a period of responsible payments.

- Graduation rewards in the form of cash rebates or interest rate reductions.

- Referral bonuses for recommending the lender to others.

- Early repayment incentives that provide interest rate reductions or cash rebates for paying off loans ahead of schedule.

- Military discounts that offer special interest rates or repayment terms for service members and veterans.

- Employer-linked discounts that reduce interest rates or provide loan repayment assistance for employees.

- By understanding the discounts and incentives available, you can lower your interest rate, reduce your loan balance faster, and save money over the life of your loan.

8. Consider Customer Service and Support

- Customer Support: Research the lender’s reputation for customer service. Read reviews and ask your school’s financial aid office for recommendations on lenders with strong customer support.

- Online Tools: Some lenders offer useful online tools to help you manage your loan, make payments, and keep track of interest.

1. Accessibility of Customer Service

One of the most important factors in selecting a lender is how easy it is to reach customer service when you need help. You want to make sure that the lender has multiple channels of communication to cater to different preferences, whether you prefer talking on the phone, chatting online, or sending an email. Consider the following:

| Communication Channel | Description | How It Helps |

|---|---|---|

| Phone Support | Direct support over the phone where you can speak with a representative. | Provides the opportunity for personal interaction and direct problem resolution. |

| Email Support | Email support for less urgent matters or written communication. | Allows for a more detailed written record of issues and solutions. |

| Live Chat | A chat feature available through the lender’s website or mobile app. | Provides quick, real-time answers to your questions without waiting on hold. |

| Mobile App Support | Many lenders have mobile apps that offer integrated support features like FAQ sections and chat. | Makes it easier to get help on-the-go from your smartphone or tablet. |

How It Helps:

- Having multiple ways to get in touch with a lender ensures you can reach them in the most convenient way for you.

- Real-time chat and email responses are especially helpful for busy students with varying schedules.

2. Response Time

Customer service is only effective if they respond quickly when you need help. When selecting a lender, ask how long you should expect to wait for a response.

| Factor | Description | How It Helps |

|---|---|---|

| Response Time for Phone Support | How quickly can you expect to speak to a live person? Ideally, no more than 5-10 minutes. | Quick response times mean that you can resolve issues without waiting for extended periods. |

| Response Time for Email Inquiries | Lenders should respond to emails within 1-2 business days. | Faster email responses ensure that you aren’t left hanging while trying to make important decisions. |

| Live Chat Availability | Many lenders offer instant responses via live chat, especially for common questions or concerns. | Instant support allows you to get help in real-time, which is great for immediate issues like payments. |

How It Helps:

- Fast response times ensure that you don’t have to wait long to resolve urgent issues, such as billing problems or technical support.

- Long waits can cause frustration, so look for lenders that pride themselves on fast and efficient service.

9. Research Lender Reputation

Check Online Reviews

One of the first steps in assessing a lender’s reputation is to read online reviews. Borrowers often share their experiences with a particular lender, including their interactions with customer service, the clarity of loan terms, and how the company handles issues like repayment. Popular websites for checking lender reviews include:

| Review Source | Description | How It Helps |

|---|---|---|

| Trustpilot | A website that collects reviews from real customers about businesses, including student loan lenders. | Provides user feedback about customer service, loan terms, and experiences with the lender. |

| Better Business Bureau (BBB) | An organization that tracks and evaluates businesses, including their customer complaints and resolutions. | BBB ratings give you an idea of the lender’s reliability and how well they handle customer concerns. |

| Consumer Financial Protection Bureau (CFPB) | This federal agency tracks and resolves complaints about financial products, including private student loans. | Can provide official records of any complaints or issues raised against the lender. |

| Google Reviews | You can check Google reviews directly, where borrowers leave their feedback about the lender. | Helps to see ratings and reviews from borrowers who have dealt with the lender firsthand. |

How It Helps:

- Online reviews can give you a real-world perspective on the lender’s overall reputation and the experiences of other borrowers.

- Look for patterns in reviews: if many borrowers share similar positive or negative experiences, that can indicate the lender’s true service quality.

10. Read the Fine Print

- Loan Agreement: Always carefully review the loan terms and conditions. Be sure you fully understand the interest rates, fees, repayment options, and any other obligations before you sign the loan agreement.

When applying for a private student loan, it’s essential to read the fine print before signing anything. The fine print often contains important details about the terms and conditions of the loan that could have a significant impact on your financial future. Skimming through the fine print can lead to misunderstandings and unexpected costs later on. Understanding the finer details of your loan agreement ensures that you’re fully aware of your rights, obligations, and potential pitfalls.

Here’s a breakdown of key areas to pay attention to in the fine print of your private student loan agreement:

Interest Rate and How It’s Determined

The interest rate is one of the most important aspects of any loan, and understanding how it’s determined is crucial. In many cases, private student loans offer variable or fixed interest rates, but the fine print will specify how and when the rate can change. Make sure to check the following:

| Factor | Description | How It Helps |

|---|---|---|

| Fixed vs. Variable Rates | A fixed rate remains the same throughout the life of the loan, while a variable rate can change over time based on market conditions. | Understand whether your interest rate will stay consistent or potentially rise, making your payments higher. |

| Rate Caps and Floors | Some variable rate loans have caps (maximum rates) and floors (minimum rates) to limit how high or low the rate can go. | Ensure that the variable rate won’t go higher than what you can afford, especially if the market fluctuates. |

| Rate Changes and How Often | Find out how often the interest rate can adjust (e.g., annually or quarterly), and under what conditions. | Know how your payment schedule may change if the rate adjusts. Make sure it fits within your budget. |

How It Helps:

- By understanding the interest rate structure, you can plan your repayments and understand how changes in the market can affect your payments.

Also Read: How Can You Lower Your Business Loan Interest Rates to Save Money?

Conclusion:

Choosing the right private student loan is a significant decision that will impact your financial future. By following a detailed process and considering factors such as interest rates, loan terms, fees, repayment flexibility, lender reputation, and more, you can make an informed choice that aligns with your needs and goals.

FAQs

What is a private student loan?

- A private student loan is a loan offered by private lenders, such as banks, credit unions, and online lenders, to help cover the cost of your education. Unlike federal student loans, private loans are based on your creditworthiness, and the interest rates and repayment terms can vary significantly.

How do private student loans differ from federal student loans?

- Federal student loans are offered by the government and typically offer lower interest rates, more flexible repayment options, and the possibility of loan forgiveness. Private student loans, on the other hand, are provided by private institutions and often have higher interest rates, stricter eligibility requirements, and less flexibility in repayment terms.

Can I get a private student loan without a cosigner?

- It is possible to get a private student loan without a cosigner if you have a strong credit history and income, but many students without established credit will need a cosigner. A cosigner can help secure a loan with better terms and lower interest rates.

How do I qualify for a private student loan?

- Qualification for a private student loan depends on your credit history, income, and other financial factors. Lenders will evaluate your ability to repay the loan by reviewing your credit score and financial situation. If you have a limited credit history, you may need a cosigner to qualify.

What is the interest rate on private student loans?

- Interest rates on private student loans vary depending on the lender, loan type, and your creditworthiness. Private loans typically offer both fixed and variable interest rates, and your rate may be higher than federal loans, especially if you have poor credit. You can check your potential interest rate by applying with the lender or using a rate calculator.

Can I refinance my private student loan?

- Yes, many lenders offer refinancing options for private student loans. Refinancing can help you secure a better interest rate, change your loan term, or combine multiple loans into one. However, keep in mind that refinancing will remove any federal loan protections, such as deferment or income-driven repayment plans.

Are there any fees with private student loans?

- Yes, some private student loans come with fees, such as origination fees, late payment fees, or prepayment penalties. These fees can add to the overall cost of your loan, so it’s important to read the fine print and understand all associated costs before accepting a loan offer.

Related Post

How Can You Lower Your Business Loan Interest Rates to Save Money?

Running a business is an expensive venture, and securing a business loan can be a [...]

Online Business Loans: A Modern Solution For Entrepreneurs

In today’s rapidly evolving business landscape, securing financing is one of the most crucial aspects [...]